COVID-19 Impact Study on Uganda Refugee Saving Groups

Survey Methodology:

A small survey was undertaken by VisionFund Uganda (VFU) field officers between 24 April and 19 May, 2020 of refugees and host community savings group (SG) members in West Nile, Uganda. Interviews were conducted mostly face to face, with a small number conducted via phone call. Due to health considerations, the face to face interviews were carried out using social distancing, face masks and a smart phone application to digitally capture the results for analysis.

Individual group members interviewed: 417[1]. Women: 229; men: 188

Refugee: 246 and Host: 171

Locations: Obongi district (previously Moyo): 270 and Yumbe district: 147

Objective:

Understand the effect of COVID-19 on savings group (SG) on both host and refugee communities in the two districts.

Background:

In Uganda, because of COVID-19 restrictions, all meetings with more than five people are prohibited. At the same time, non-essential businesses were closed and transport limited. A normal SG has 24 - 30 members; so with the “meeting in small groups” restriction they are meeting in groups of five to get their savings and then through the group leaders consolidating these funds into the savings box.

VFU has been working in Obongi district since May 2019 and has disbursed US$ 92,000 to 100 savings groups, supporting 2,264 individual group members. VisionFund started training saving groups in Yumbe district late 2019, but has not financed any group yet. Savings groups have been operating in both districts for some time and all the interviewed groups have been in existence for at least two cycles (or two years). VFU is the first MFI to offer loans into those groups. It should be noted that this survey was primarily looking at how savings groups have been impacted and not the loans from VFU.

It should also be noted that prior to the survey, the refugee camps had a reduction in food rations due to funding shortages in WFP. Often those food rations were sold and contributed to additional income for the households. With the lockdown, they have lost that income.

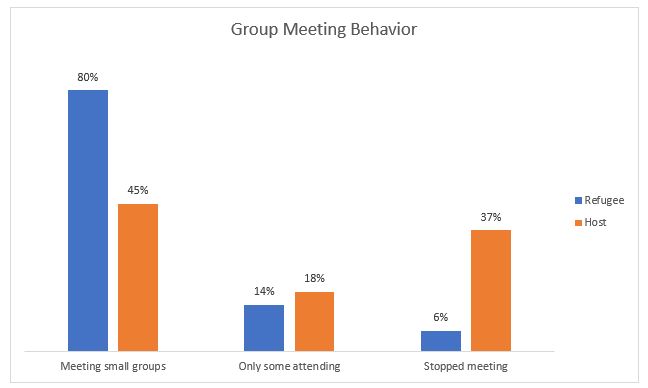

Savings Group Meeting Behavior

The majority (81%) of the groups are still meeting; only 19% of groups have stopped meeting. The main strategy has been to keep meeting (65%), but in small groups as per government requirements on social distancing. One explanation for the stronger resilience of the refugee groups may be that these groups had more support in their formation than host groups.

[1] This study is about the impact of COVID-19 on saving groups in both host and refugee communities. In the two areas we looked at (Moyo and Yumbe), most saving groups in Moyo had already received financial services while in Yumbe individuals had received financial literacy training but no loans.

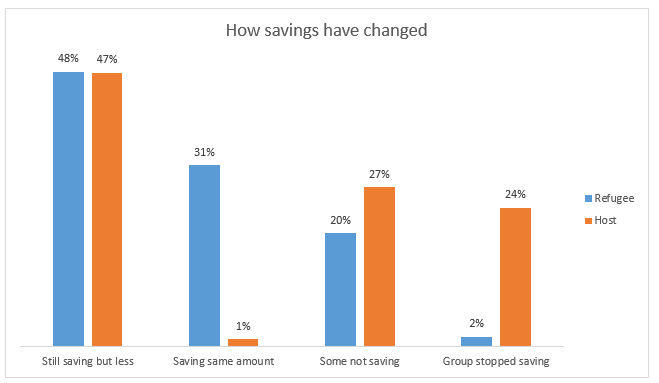

Almost all refugee groups are still saving (some are saving less) while 24% of host groups have stopped saving. The conclusion is that refugee groups have not only adapted to the new meeting guidelines but have also found ways to continue meeting, showing higher levels of resilience.

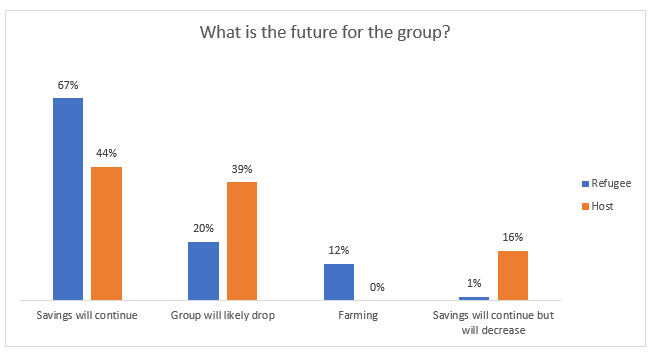

When asked about the future of the group, of the overall 417 participants 65% expected to continue to save. However, it is worrying that 28% of all respondents expected to drop and for host communities this was up to 39% of respondents. We need to better understand what this means long term, along with the shift to farming in the chart below.

Impact on Households

Households were stressed on two fronts. 88% of all respondents reported an increase in staple food prices, which puts pressure on household budgets. Almost all refugee respondents (96%) reported the increase, which probably reflects the reduction of their WFP rations. At the same time, 92% of all respondents reported some level of financial stress due to either lower business activity (34%), decreased income (23%), challenges to save (25%) and food insecurity (11%). It’s safe to conclude that all households were stressed by the COVID-19 pandemic, but even though refugees were stressed at a higher level, they proved to be more resilient.

Despite these stresses, households are not resorting to increased demand for the SG social fund or selling their assets (87% haven’t had to sell any assets). In terms of demand on the savings group social fund, 58% of the groups reported no change in number of requests (with little difference between host and refugee), but did note that those who did request use of the social fund, the amount was significant.

Business impact

Savings group members engage in multiple economic activities. Similar to other studies on the impact of COVID-19, 93% of all respondents reported some level of reduced income. More than half of the groups reported either a big reduction in income (47%) or a complete stop to income (11%). Interestingly, 6% reported an increase in income reflecting that there are business opportunities even in a crisis.

Resilience

A last question asked how groups were adjusting their businesses due to the COVID-19 crisis, this shows a range of different activities that households are doing to survive. This again shows how refugees are adjusting in various creative ways to the stresses they are facing.

Conclusion

This report would like to make the following three points:

- Refugee savings groups are resilient: The demonstrated resilience of these refugee savings groups (compared to host groups) continues to support the thinking that the formation and support for refugee savings groups is a key response to livelihoods for long term refugee communities.

- COVID-19 is having a dramatic impact on the livelihoods of the rural poor: This survey was undertaken in a remote part of Uganda which supports anecdotal evidence that rural communities are as much impacted as the more visible impacts of COVID-19 on people livelihoods.

- Surveys can be done safely in a lockdown situation: Finally, this report shows that even in a lock down situation, using a simple digital tool and practicing social distancing guidelines surveys can be done quickly.

[1] This study is about the impact of COVID-19 on saving groups in both host and refugee communities. In the two areas we looked at (Moyo and Yumbe), most saving groups in Moyo had already received financial services while in Yumbe individuals had received financial literacy training but no loans.

Authors: Martina Crailsheim, Refugee Finance Programme Manager, VisionFund Uganda and

Dr. Richard Reynolds, Global Director Products and Innovation, VisionFund International